Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Larry is Farcaster's silver shovel?

Recently, innovations in asset issuance methods on Base have continued to emerge: "Can you really play Base Clanker?", many new products have emerged in the community, and Larry is one of the most distinctive ones.

At 12 noon on December 5, David Fulong (@df), senior developer of Farcaster and founder of Frame protocol, published a cast, announcing the birth of Larry.

Team background: Larry vs Clanker

Clanker was founded by @_proxystudio and @JackDishman, and Larry was founded by @davidvfurlong and @stephancill.

Farcaster veteran player @0xLuo popular science: Clanker's founding team is a new developer of Farcaster, Larry's founding team is Farcaster OG, @davidvfurlong's resume is particularly impressive: his company has received investment from A16Z (note that A16Z did not invest in Larry), and he himself is also the proposer of the Frame protocol - Frame is a major innovation of Farcaster, and it is also the key to the Farcaster team's ability to get $150 million "on the surface".

In contrast, Larry's team is more politically successful; but Farcaster's OG status is a negative buff for the publisher, after all, it is well known that Farcaster is a mosque...

From an operational perspective, Clanker does understand memes better. Its founder @proxystudio.eth often contributes various "god comments" to Farcaster, and Clanker's official account (@_proxystudio ) is also very funny:

On the other hand, Larry, maybe because it was just launched less than a week ago, the entire team's energy was completely focused on product development and mechanism design, and there was almost no support for ecological projects and operation of official brands and communities - this is an important reason why its leading token $LARRY (currently around 3M, up to 7M) lags far behind Clanker's leading token $CLANKER (currently around 50M, up to 150M) in market value.

Asset Issuance Mechanism: Larry vs Clanker

In a nutshell, Larry and Clanker are both AI Agents that issue tokens as soon as they post. Larry’s asset issuance method imitates Pumpfun’s internal and external pool mechanism, while Clanker’s asset issuance method is fair launch - the former’s shortcoming is that the threshold restricts retail investors from participating in the early stage, while the latter’s shortcoming is that it is difficult to overcome robot sniping.

Asset issuance mechanism: Clanker

Specifically, by tagging Clanker on Farcaster and stating the token name, ticker, and header image, Clanker can add a Uniswap pool with a starting market value of approximately $30,000 on Base for free (the threshold is that the Farcaster account Neynar score must be high enough, which means it is difficult for newcomers to issue tokens). All deployed tokens can be viewed on the official website.

Unlike PumpFun, which charges 1% transaction fee + 2 Sols on Raydium fee during the bonding curve, Clanker does not have a bonding curve, but charges 1% handling fee from Uni v3 as income: 40% to the issuer and 60% to the Clanker team - this split ratio may change, see official documentation for details.

Asset issuance mechanism: Larry

Like Clanker, Larry also issues tokens by posting with a threshold limit.

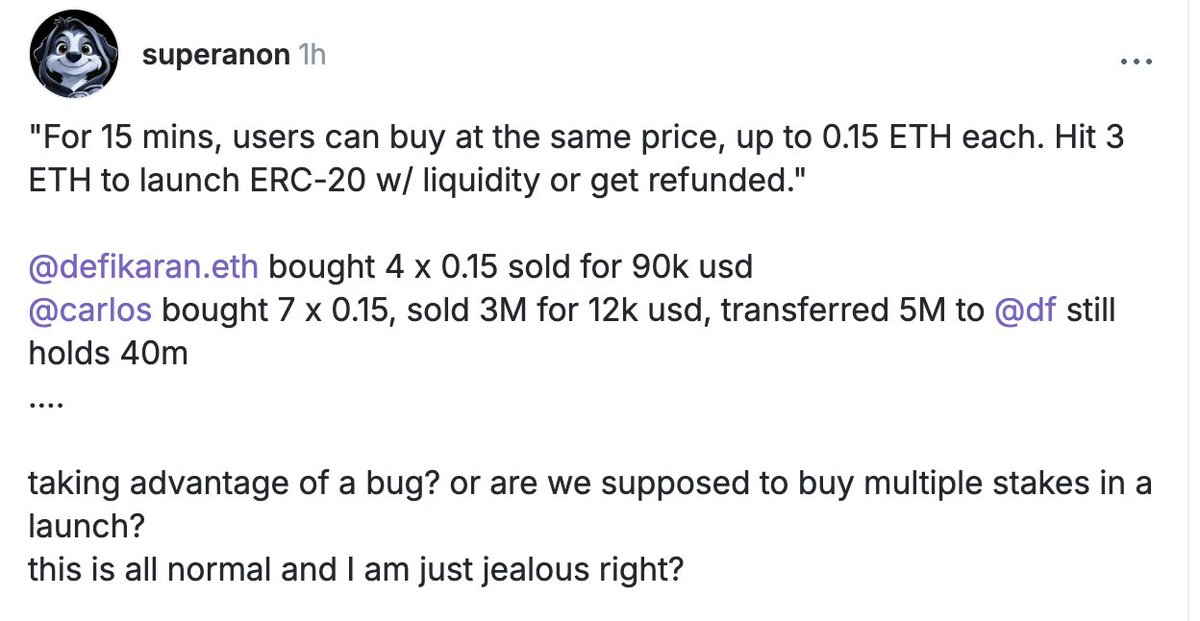

After receiving the message, Larry AI Agent will initiate an internal market on its official website Larry.club : The latest rule is that the upper limit of the internal market fundraising time is changed to 69 minutes, each person can put in a maximum of 0.25E, and all people can put in a total of 3E. After it is full, it will wait for a while before adding a pool to open on V3. (Previously it was 15 minutes and over-subscription was allowed)

The specific details are that a launch button will appear on the page, and then an internal user is required to confirm and pay the gas fee (Note: the dev sold displayed on GMGN is actually the user who clicked the launch button, not the real developer...)

A very criticized point in the whole mechanism is that the neynar score needs to be higher than 0.8 to fill the internal plate, and ordinary retail investors can't get in at all. They can only watch Farcaster OGs fill the internal plate and then take their chips on the external plate - in fact, they can understand the intentions of the mechanism designers: after all, this is an era where whoever has the bottom chips is the dealer, and the team hopes that the "dealers" will cherish their feathers and not smash them as soon as the market opens - but the reality is: many plates on Larry are drilled into the ground in 10 seconds, because people on the internal plate know how bad the experience of people on the external plate is. If the angle is not tricky enough, no one will come to take it, thus forming a stampede on the internal plate...

Currently The voice of FUD Larry tokens is dominant. Apart from the leading $LARRY, no other token can survive the second wave of drilling, let alone take off like $ANON $CLANKER $LUM on Clanker... (For the launch of various tokens on Larry in the past few days, see this tweet)

But it’s still early days, the mechanism design may change at any time, and the team is also constantly thinking about how to best couple the internal mechanism with the real-name PVP Socialfi game - let us continue to observe. (For a more detailed comparison between Clanker and Larry, see this tweet.)

Larry’s development history: from drilling into the ground to V-reversal

BUG storm: explosive pull and then drilling into the ground

Open the candlestick chart of $LARRY, you will find that it pulled up on the first day, and then continued to drill into the ground for the next two days.

(Note again: the dev sold shown on GMGN is actually the user who clicked the launch button, not the real developer)

Why? The most important reason is that Larry's software crashed at the beginning. On the one hand, it could not issue coins. On the other hand, it was caught in a public opinion storm that the software had a bug and introduced internal insider trading: An anonymous person claimed that two participants used 0.6 ETH and 1.05 ETH at the bottom to sell when the market was rising, and each earned 90k and 12k...

The founder @davidvfurlong admitted the software bug and apologized, and then fixed the vulnerability. He also kept fixing bugs for the next two days, which was quite embarrassing: the coin price plummeted all the way, from a high of 7M to less than 1M...

Continuous construction: drilling is rising again

BUG After repairs and mechanism optimization, the K-line of Drilling has risen again, and is currently fluctuating between 2M and 4M.

Two days ago, the founder @davidvfurlong did another big thing: he released a Farcaster AI template as an open source for later developers to quickly deploy AI Agents on Farcaster, which led to a series of AI Agents interacting with Larry, including the dqau (the corresponding token is @freysa_ai "man-machine game" story that went viral on Twitter) reproduced on Farcaster.

Where is Larry's future?

The editor observed the community and found that the evaluation of Larry by community members can be summarized in eight words: "Sorry for his misfortune, angry at his lack of competition."

"Sorry for his misfortune" means that Larry's release did not cater to the right time: on the day of Larry's release, Clanker was making a fortune and was in the limelight; in addition, the liquidity of the Farcaster ecosystem was far from sufficient for people to chase the second dragon; and who would have thought that the products of the two super developers would have a lot of bugs as soon as they went online - the leading token $LARRY and its ecological tokens were continuously suppressed, and many "precious angles" were wasted...

"Angry at his lack of competition" means that Larry's team is too pure, does not know how to make things, and more importantly, does not know how to make markets - this is actually a common problem of all Farcaster tokens.

This wave of memes is a key step in the process of Farcaster's de-halalization. People will gradually flock in: from the lone P players to the real dealers, who can only pull up the lever to bring about a flood of money - I hope this day will come soon.

You may also like

Stolen: $290 million, Three Parties Refusing to Acknowledge, Who Should Foot the Bill for the KelpDAO Incident Resolution?

ASTEROID Pumped 10,000x in Three Days, Is Meme Season Back on Ethereum?

ChainCatcher Hong Kong Themed Forum Highlights: Decoding the Growth Engine Under the Integration of Crypto Assets and Smart Economy

Why can this institution still grow by 150% when the scale of leading crypto VCs has shrunk significantly?

Anthropic's $1 trillion, compared to DeepSeek's $100 billion

Geopolitical Risk Persists, Is Bitcoin Becoming a Key Barometer?

Annualized 11.5%, Wall Street Buzzing: Is MicroStrategy's STRC Bitcoin's Savior or Destroyer?

An Obscure Open Source AI Tool Alerted on Kelp DAO's $292 million Bug 12 Days Ago

Mixin has launched USTD-margined perpetual contracts, bringing derivative trading into the chat scene.

The privacy-focused crypto wallet Mixin announced today the launch of its U-based perpetual contract (a derivative priced in USDT). Unlike traditional exchanges, Mixin has taken a new approach by "liberating" derivative trading from isolated matching engines and embedding it into the instant messaging environment.

Users can directly open positions within the app with leverage of up to 200x, while sharing positions, discussing strategies, and copy trading within private communities. Trading, social interaction, and asset management are integrated into the same interface.

Based on its non-custodial architecture, Mixin has eliminated friction from the traditional onboarding process, allowing users to participate in perpetual contract trading without identity verification.

The trading process has been streamlined into five steps:

· Choose the trading asset

· Select long or short

· Input position size and leverage

· Confirm order details

· Confirm and open the position

The interface provides real-time visualization of price, position, and profit and loss (PnL), allowing users to complete trades without switching between multiple modules.

Mixin has directly integrated social features into the derivative trading environment. Users can create private trading communities and interact around real-time positions:

· End-to-end encrypted private groups supporting up to 1024 members

· End-to-end encrypted voice communication

· One-click position sharing

· One-click trade copying

On the execution side, Mixin aggregates liquidity from multiple sources and accesses decentralized protocol and external market liquidity through a unified trading interface.

By combining social interaction with trade execution, Mixin enables users to collaborate, share, and execute trading strategies instantly within the same environment.

Mixin has also introduced a referral incentive system based on trading behavior:

· Users can join with an invite code

· Up to 60% of trading fees as referral rewards

· Incentive mechanism designed for long-term, sustainable earnings

This model aims to drive user-driven network expansion and organic growth.

Mixin's derivative transactions are built on top of its existing self-custody wallet infrastructure, with core features including:

· Separation of transaction account and asset storage

· User full control over assets

· Platform does not custody user funds

· Built-in privacy mechanisms to reduce data exposure

The system aims to strike a balance between transaction efficiency, asset security, and privacy protection.

Against the background of perpetual contracts becoming a mainstream trading tool, Mixin is exploring a different development direction by lowering barriers, enhancing social and privacy attributes.

The platform does not only view transactions as execution actions but positions them as a networked activity: transactions have social attributes, strategies can be shared, and relationships between individuals also become part of the financial system.

Mixin's design is based on a user-initiated, user-controlled model. The platform neither custodies assets nor executes transactions on behalf of users.

This model aligns with a statement issued by the U.S. Securities and Exchange Commission (SEC) on April 13, 2026, titled "Staff Statement on Whether Partial User Interface Used in Preparing Cryptocurrency Securities Transactions May Require Broker-Dealer Registration."

The statement indicates that, under the premise where transactions are entirely initiated and controlled by users, non-custodial service providers that offer neutral interfaces may not need to register as broker-dealers or exchanges.

Mixin is a decentralized, self-custodial privacy wallet designed to provide secure and efficient digital asset management services.

Its core capabilities include:

· Aggregation: integrating multi-chain assets and routing between different transaction paths to simplify user operations

· High liquidity access: connecting to various liquidity sources, including decentralized protocols and external markets

· Decentralization: achieving full user control over assets without relying on custodial intermediaries

· Privacy protection: safeguarding assets and data through MPC, CryptoNote, and end-to-end encrypted communication

Mixin has been in operation for over 8 years, supporting over 40 blockchains and more than 10,000 assets, with a global user base exceeding 10 million and an on-chain self-custodied asset scale of over $1 billion.

$600 million stolen in 20 days, ushering in the era of AI hackers in the crypto world

Vitalik's 2026 Hong Kong Web3 Summit Speech: Ethereum's Ultimate Vision as the "World Computer" and Future Roadmap

On the same day Aave introduced rsETH, why did Spark decide to exit?

Full Post-Mortem of the KelpDAO Incident: Why Did Aave, Which Was Not Compromised, End Up in Crisis Situation?

After a $290 million DeFi liquidation, is the security promise still there?

ZachXBT's post ignites RAVE nearing zero, what is the truth behind the insider control?

Vitalik 2026 Hong Kong Web3 Carnival Speech Transcript: We do not compete on speed; security and decentralization are the core

In-depth Analysis of RAVE Events: Short Squeeze, Crash, and Quantitative Financial Models of Liquidity Manipulation